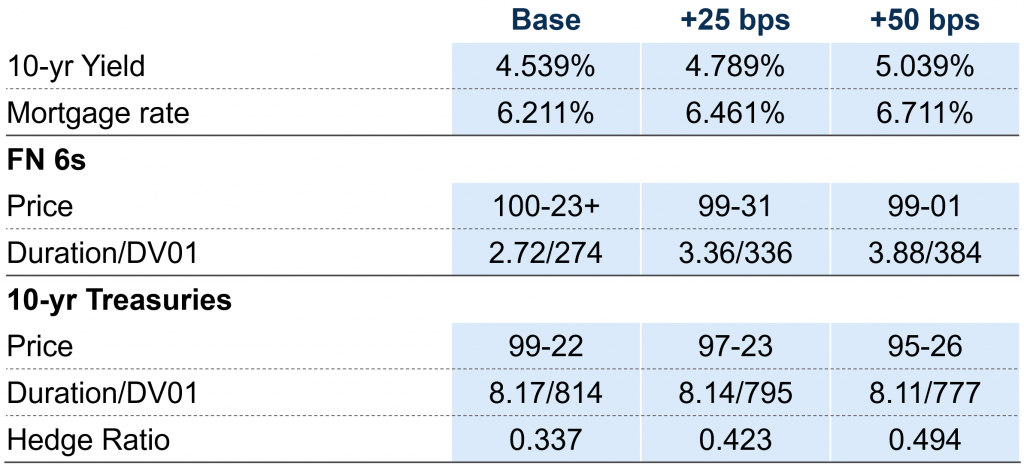

We Hedge Yield Deltas With Treasury Duration

We have access to private Treasury and Agency debt markets where firms trade trillions of dollars worth of notional contracts per day. We use industry standardized formulas to measure changes in rate sensitivity, then conduct systematic analyses of outcomes from reasonably foreseeable changes in rates before each order that we place. This helps us stay in precise control of our risk exposure at all times so as to execute trades with little or no position or rate risk. Incomes from such trades are appended to our ordinary business income returns from REIT operations.